Benchmarking BC's sub-GIs

Karen Graham has written an interesting and informative blog on BC's new sub-GI announcements (https://lnkd.in/gf7jwp-2). I certainly agree with her premise that these are "aspirational". The first sub-GI was Golden Mile Bench in 2015 and the next tranche happened very slowly. Now we have added 7 in 2022, Golden Mile Slopes (GMS) was launched without any fanfare in January and six just now.

East Kelowna Slopes (EKS), South Kelowna Slopes (SKS), Lake Country (LC), Summerland Bench (SUMB), Summerland Lakefront (SUML), and Summerland Valleys (SUMV).

We now have eleven sub-GI within the Okanagan Valley DVA and one on Vancouver Island. The chart shows all twelve. There is an application for the 13th in process - "Black Sage Bench".

The principal goal of a sub-GI is the definition of grape source. BC wineries located in, say, Naramata can make wine Golden Mile Slopes grapes and label the wine as "Golden Mile Slopes", subject to the rules around labeling and content. The data more properly represents in which sub-GI the wine is made rather than necessarily grown. But since sub-GIs are recent, most consumers associate the brand with the sub-GI rather than the grape source. It will take many years of consumer education to separate the two. It may also take a radical overhaul of how wineries based in a sub-GI actually make and how their brands are marketed.

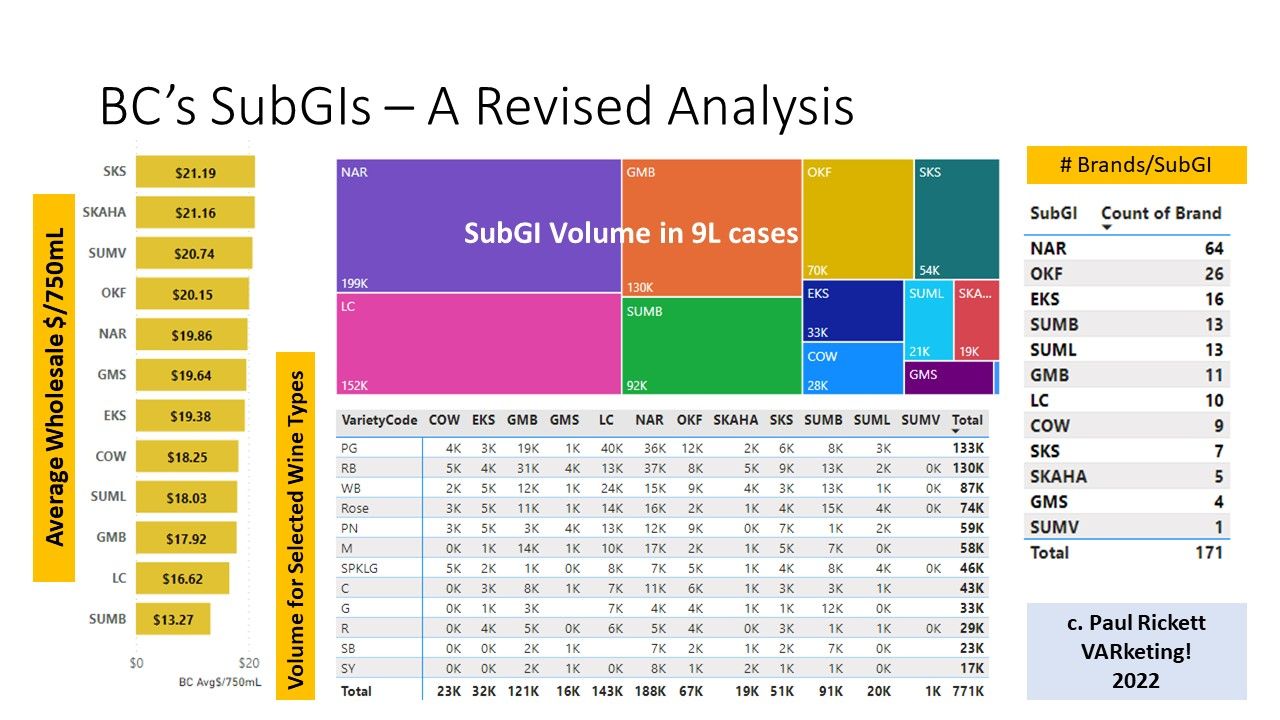

Very kindly she included a screenshot from #BCwine2021 that predated the new sub-GIs. I have re-categorised and extended the data to reflect these in the chart below:

* Average Price is WHOLESALE price weighted by volume for only 750mL format sales within BC (Karen's version was for all formats).

* Area chart provides total 750mL 9L case volume.

* Table below gives case volume by principal wine types. These represent a subset of the total volume sold. This data more properly represents in which sub-GI the wine is made.

* Table on right is # of Brands by wineries located in the sub-GI. "Brands" are a new enrichment of the data based on selected tiering criteria. Logically, there are more brands than wineries, although for most small wineries there is a one-to-one relationship. Not all larger wineries have multiple "brands" either.