A Taxonomy of the BC Wine Industry

This post is about the structural make-up of the BC wine industry and how it has been interpreted into our data analysis. Most structural metrics focus around the number of BC wineries registered - and whether they are licensed as Estate or Commercial. For the purposes of VARketing's BC wine analytics I have redefined and regrouped the data into a slightly different hierarchical sequence than that of the licensed supplier shown in LDB data. This allows more precise and flexible analysis and in turn allows additional attributes that are useful in comparing trends and performance over time.

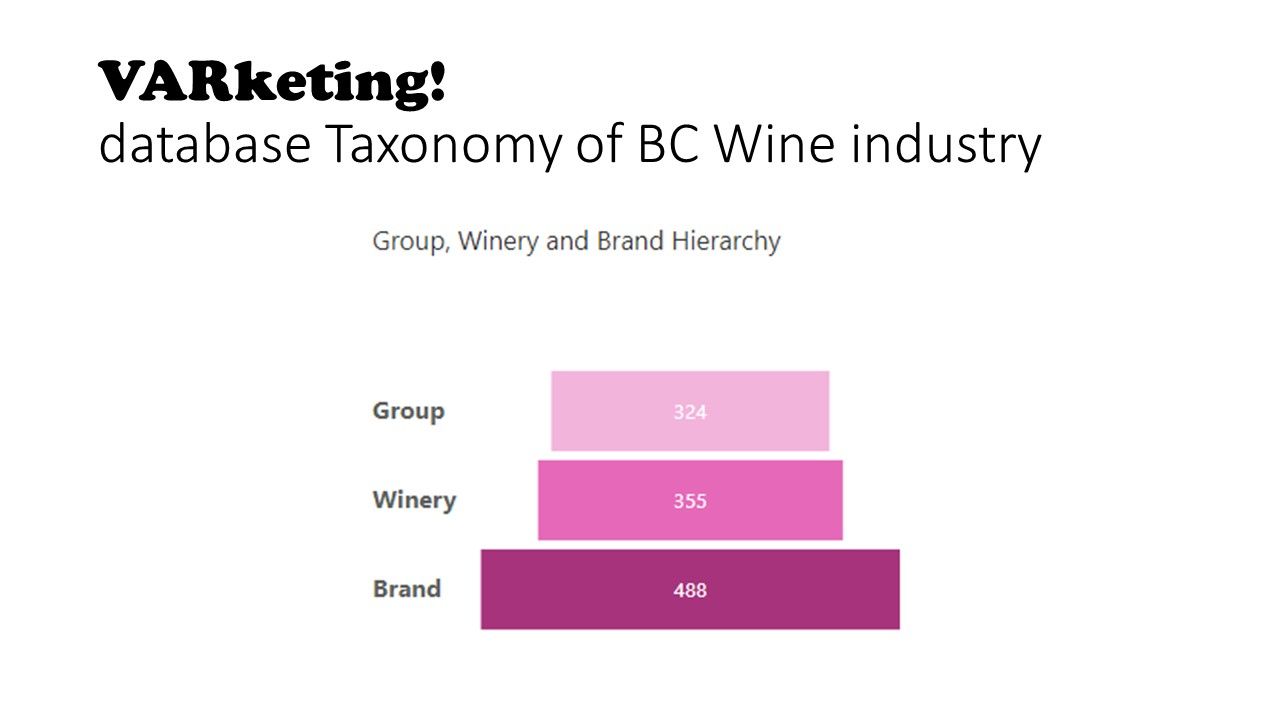

The three key hierarchical terms used are:

- Group

- Winery

- Brand

Groups:

The highest level in the hierarchy. The group definition is based on common ownership. The obvious examples, and largest, are the various wineries and brands owned by Arterra, Mark Anthony, and Andrew Peller (collectively known as the "Big 3"). These operate a combination of physical (i.e., visitable) wineries and virtual brands. Some of their virtual brands are composed of wines made that are solely ICB (and are excluded from below), some that have both mixed and ICB products and some that are purely 100% BC content - in most (but potentially not all) of these brands those products that are 100% BC do carry the VQA labeling - all of these are included insofar as they have 100% BC content.

While these three are the largest, over the years, there is a slowly increasing but still very small number of Independently owned Groups where multiple wineries share common ownership. The most recent Group formation being that of Burrowing Owl with its acquisition of Wild Goose.

All Wineries (see below) are allocated to their own group which accounts for the high number of groups. In practice, the total number of Groups containing multiple Wineries is numbered in single digits.

Wineries:

This is the nearest direct equivalent of the number of licenses but it is not completely the same. For the purposes of our analytics a winery is a collection of Brands owned, made, and distributed by a licensed winery. Independent Virtual wineries are counted as a separate Winery and treated for all comparisons as a stand-alone independent winery over the time period even though its wines were, for regulatory purposes, included and accounted for by the manufacturing winery. For instance, Seven Directions is now a licensed, physical winery, in the past its wines were made by other wineries.

The upshot here is that a licensed winery may actually produce more wines than we would show if it was contract manufacturing on behalf of a third party. The principle adopted here is that while contract manufacturing may provide economical benefits to the winery, it is not an expression of the winery's Brand(s).

The second adjustment concerns virtual brands made by the 'Big 3'. These virtual brands are grouped under a generic winery name within the Group. This adds 3 wineries to the total.

Wineries may have Attributes. One Attribute series is commonly used to segregate Independent wineries and brands from those of the Big 3.

I have started adding new experimental Attributes to track various scores that are not specifically product related (e.g. Google and TripAdvisor scores) plus broad physical characteristics such as co-located restaurant, tasting room scale and style. The BC's Winemakers database also links at this level.

Brands:

These are really the core of the hierarchy and the primary analytical layer. A Brand is an elastic concept rather than rigidly defined. A Brand is generally either a substantial and/or distinct tier in a winery's spectrum of offerings. The term 'distinct' is flexible and will evolve but is based primarily on how a brand is communicated to a consumer. This means that a Brand with substantially the same label design regardless of its own concept of a tier (e.g., adding a Reserve wine with substantially the same marketing approach as its main products) marketed on the same website is typically treated as one Brand unless the volume of the tier is a substantial component of the winery's sales or there is a compelling reason to segregate it. As stated previously, this is an elastic concept and can be modified as needed for clients. A Winery may have multiple Brands.

Brands can also be far more volatile than a Winery. The Winery layer gets incremented with new licenses being added. Closed wineries are maintained for history tracking so are not removed. Brands, however, can grow, shrink or even disappear as winery strategy evolves. The Brand indicator is also used to segregate private label distribution from the main consumer Brand(s).

Brands can have Attributes too. At present there are three attributes.

- Differentiate whether the Brand is based on a physical winery (i.e., a consumer can expect to be able to purchase the Brand when visiting the tasting room) or is completely separated from the physical.

- Brand Maturity - volume and longevity of the Brand within our data. More on this in upcoming posts.

- Brand Status - active, closed or future (wineries/brands that are just opening and have no sales within the 2016-2021 time period but will have activity in 2022 onwards.

The Brand acts as the linkage between product level data and the Winery and Group layers.

For most, especially small, wineries there is a 1:1:1 relationship between Group, Winery and Brand.

This taxonomy provides a structure for flexible analysis of the SKU level data we track. The graphic at the top of the post shows the total numbers in each layer currently being tracked.

There are a few larger wineries for which I have not yet made a decision on how to segregate, or even if to do so, elements of their production into Brands. Creating new 'Brands" in these cases should have no material impact on the upcoming analysis by Brand maturity as in all cases the revisions will fall into the same category and will not change overall results.